In 2021, a typical family does not exist in the way that it used to. Every family is different; some people remarry, have stepchildren, adopt children. However, the laws surrounding inheritance do not reflect this. According to reports, unofficially adopted children are treated unfairly in inheritance matters. This is because there are certain rules surrounding inheritance tax depending on your relation to the deceased.

Different Rules for Unofficially Adopted Children

One of the rules that is different for children related by blood and unofficially adopted children is the Residence Nil Rate Band. With the Residence Nil Rate Band, each individual has an allowance regarding inheritance tax. Currently, the value is £325,000 – but if you have a property or if you have owned a property, and in your will, you leave your estate to your direct descendant, then you may claim an additional threshold before inheritance tax of £175,000, bringing the total allowance to £500,000. You do need to meet other certain criteria to claim this extra allowance.

However, the Residence Nil Rate Band – although it includes stepchildren or foster children – excludes people who have not got children but want to leave it to nieces and nephews or persons who they view as a child.

This means that unofficially adopted children must pay more inheritance tax than children or stepchildren.

Dying Intestate

There are also problems when someone dies without making a will – also known as Intestacy Rules.

If this is the case, it completely and utterly excludes unofficially adopted children and even stepchildren. If you die without making a will, you must follow the Intestacy Rules and that does not even include stepchildren.

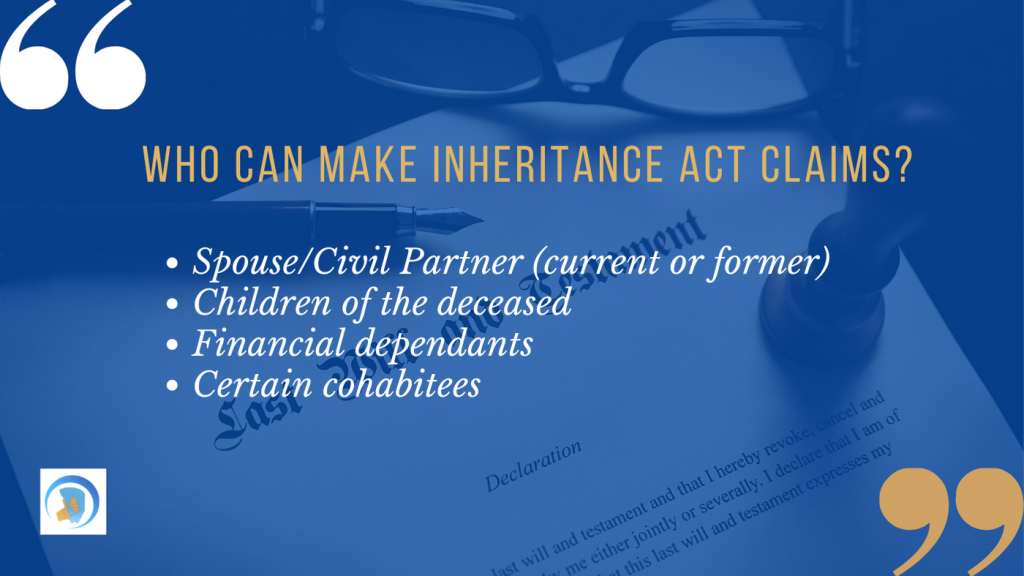

Inheritance Act Claims for Unofficially Adopted Children

The Inheritance (Provision for Family and Dependants) Act 1975 states that it is

“An act to make fresh provision for empowering the court to make orders for the making out of the estate of a deceased person of provision for the spouse, former spouse, child, child of the family or dependant of that person; and for matters connected therewith.”

Put simply, this act ensures that when a person passes away, every beneficiary receives part of their estate. A beneficiary is anyone who receives anything in a Will.

Certain people, if a Will does not include them, and they believe it should, may be able to make an Inheritance Act claim. So if they believe that they were wrongly left out of a Will, they may be able to make a claim.

How We Can Help with Unofficially Adopted Children being Treated Unfairly in Inheritance

Here at The Inheritance Experts we work with solicitors who have years of experience dealing with inheritance claims. This includes claims for unofficially adopted children being treated unfairly in inheritance. Contact us today by filling in our contact form. Or call us on 01614138763 to speak to one of our friendly knowledgeable advisors.